Green financing tools for the french maritime industy

a necessity to safeguard and develop the sector in the context of unfair competition

July 2022

download our position paper

Background elements

The shipbuilding industry in France accounts for a turnover of approximately €12 billion and 45,000 jobs. It integrates the entire value chain, including lead shipyards, equipment manufacturers, subcontractors, engineering firms, etc., and is capable of managing a vessel’s entire lifecycle—from design and construction to optimal technical operation and decommissioning. The shipbuilding industry is deeply rooted in coastal regions and sustains entire ecosystems through its construction activities, driving the economic vitality of the cities and regions where they are located.

The shipbuilding sector faces numerous economic, social, and technological challenges. Unfair foreign competition from outside the European Union market has weakened French shipyards’ ability to export and to sell to their own shipowners. The latter often prefer lower-cost yards with unfair practices, even if it means bypassing certain regulations specific to shipbuilding in France. A recent example is the purchase of a fishing vessel in Morocco, which was imported into France as a leisure craft before changing its designated use to evade certain regulations that would have incurred additional costs for the owner.

To enable the national industry to remain a global leader in shipbuilding, several State tools must be created or adapted. Various measures were highlighted during the ‘Fontenoy du Maritime’ summit, which we welcome—notably the simplification of green tax depreciation (suramortissement vert) and the combining of leasing with internal guarantees. These improvements were necessary but remain insufficient.

Three tools warrant further study and development through State-Industry dialogue:

- The rapid implementation of a support mechanism to finance the additional costs of purchasing and installing green technologies on board vessels.

- The modification of the OECD Arrangement on officially supported export credits for export programs.

- The development of tax leasing.

This note aims to elaborate on the first of these tools.

the rapid implementation of support mechanism

For the financing of additional costs related to the purchase and installation of green technologies on vessels

The maritime sector is currently responsible for nearly 3% of global greenhouse gas (GHG) emissions. 90% of global trade is carried by sea, with vessels still primarily running on heavy fuel oil1. This observation has led authorities to strengthen the regulatory framework regarding the reduction of atmospheric emissions (pollutants and GHG) for the maritime industry. The most significant milestone was the International Maritime Organization’s (IMO) adoption in April 2018 of a strategy to reduce GHG emissions from the global fleet by 50% by 2050 compared to 2008; these targets are set to be further tightened soon. Added to this objective are those of the European Green Deal (EGD), which aims for a general economic reduction of -55% in emissions by 2030 and -90% by 2050, compared to 1990 levels. As they are designed to operate for 30 to 40 years, both newly ordered and existing vessels2 must integrate technologies capable of meeting the 2050 IMO and EGD targets or be prepared to adapt to forthcoming technologies.

Achieving these goals will require significant investment in new ‘green’ technologies, particularly the use of low or zero-carbon alternative fuels. Key technologies include fuel cells, wind-assisted propulsion systems, storage tanks and delivery systems for alternative marine fuels (notably liquid hydrogen, methanol, ammonia, and LNG), energy-saving and recovery systems, and batteries. It is important to note that these investments will cover not only the development and ‘marinization’ of these technologies but also their industrial upscaling3, through to their installation on various types and sizes of vessels, including the large passenger ships built by Chantiers de l’Atlantique (CdA). Indeed, in shipbuilding, innovation is mostly implemented on board vessels in actual commercial operations, rather than on unsold prototypes.

This investment effort for the greening of large commercial vessels is particularly problematic in Europe today. European shipyards structurally have little financial leeway, and their clients—mostly cruise ship owners—are emerging from the COVID-19 health crisis heavily burdened with debt. The additional costs associated with these ‘green’ technologies represent up to 20% of the total ship cost for high-value vessels like passenger ships and can exceed 50% for lower-value vessels like merchant ships. Securing new orders for ‘green’ ships therefore appears highly uncertain and requires a support mechanism, at least temporarily, to reactivate investment and secure the order books of shipyards, including Chantiers de l’Atlantique, beyond 2025.

1. Maritime transport is the most efficient transport solution from both an economic and ecological perspective (despite the primary use of heavy fuel oil). This is why it accounts for such a significant share of global trade while representing a relatively small portion of GHG emissions compared to other industries (see Appendix 1).

2. In order to meet the 2030 and 2050 targets, the IMO is implementing increasingly stringent intermediate objectives (EEDI, EEXI, and CII indices). Consequently, as of 2023, the energy intensity of existing ships must be substantially improved across all vessel types, with particularly demanding requirements for container ships (-20% to -50% depending on size), posing a significant challenge for shipowners starting today.

3. Most of these technologies have an insufficient level of maturity and have not yet entered a cost-reduction trajectory, which is essential for competitive large-scale commercialization.

what europeans are doing ?

The Italian recovery plan includes a specific €800 million strand for financing green ships between 2021 and 2026 4 within the sustainable mobility plan. This support mechanism will primarily benefit the shipbuilder Fincantieri, which is already using it as a commercial argument with potential ship owning clients.

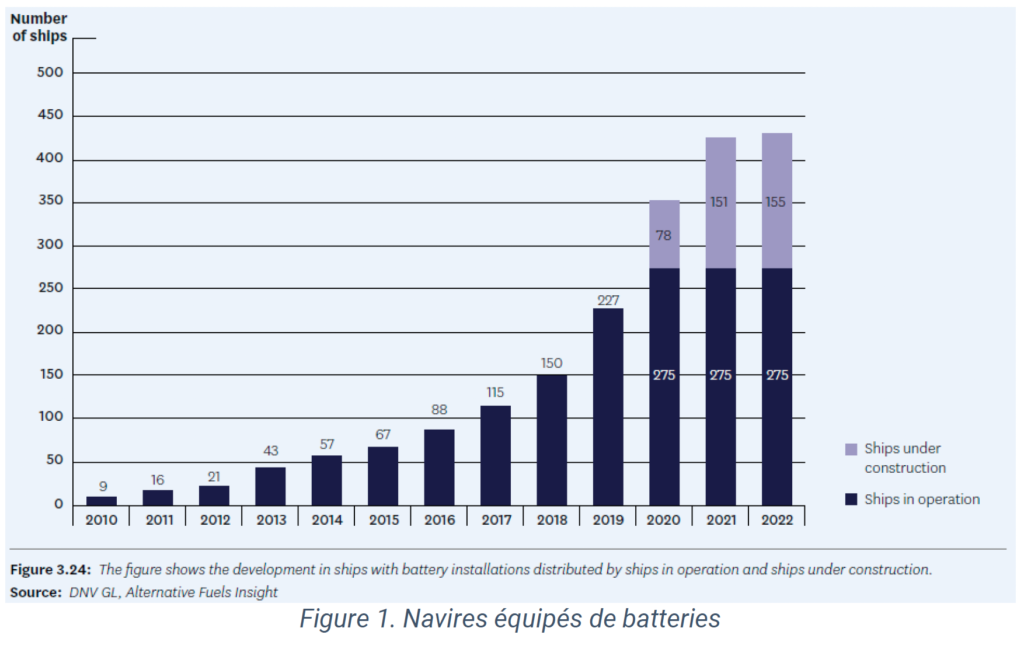

Norway established the ENOVA fund, which in 2018 provided over €200 million for green technology, including a €10 million hydrogen-powered coastal vessel project . Since its inception, Enova has supported the installation of batteries and energy efficiency systems on 155 vessels, equivalent to over €140 million in support—contributing to the financing of nearly half of the world’s battery-powered ships.

In 2020, Enova provided €26 million for two liquid hydrogen vessel projects5.

A ‘Green Deal on Maritime and Inland Shipping and Ports’ 6 was established between the central government, regions, trade organizations, shipowners, industrial players, and ports. Key actions include a shared goal to explore ways to finance GHG reduction projects for inland and seagoing vessels. Existing schemes include the ‘Sustainable Innovative Shipbuilding Subsidy’ (SDS), targeting construction and retrofit yards proposing innovative projects.

4 PNRR Piano Nazionale di Ripresa e Resilienza : https://www.governo.it/sites/governo.it/files/PNRR.pdf

5 Enova Annual Report2020

6 https://www.greendeals.nl/sites/default/files/2019–11/GD230%20Green%20Deal%20on%20Maritime%20and%20Inland%20shipping%20and%20Ports.pdf

Finland7 and the Netherlands8 have both created specific financing lines for the devlopment of clean energy on ships.

In Germany , The Ministry of Transport and Infrastructure promotes the use of LNG as a marine fuel under the government’s Mobility and Fuel Strategy 9, aiming to reduce emissions and improve air quality in ports. Additional investment costs are supported up to 40-60% of eligible costs depending on company size, with a maximum of €8 million per equipment item and retrofit project. A total budget of €278 million is targeted for shipowners choosing LNG by the end of 202110. Other energy sources are also supported.

The subsidy scheme for the installation of alternative technologies for environmentally friendly on-board and mobile shore-side power offers 40% aid (60% for SMEs) for additional investment costs11.

limitations of existing financing machanisms

European shipbuilding differs from other industrial sectors12 due to the size of the structures it produces in very limited series (fewer than ten units), their high degree of complexity, their value (over €1bn for the largest cruise ships), and the commercial use of prototype vessels (the first-in-class). Consequently, industrial scale effects are reduced. Compared to the automotive and aerospace industries, it takes longer to reach the volumes required for cost reduction and competitive commercialization.

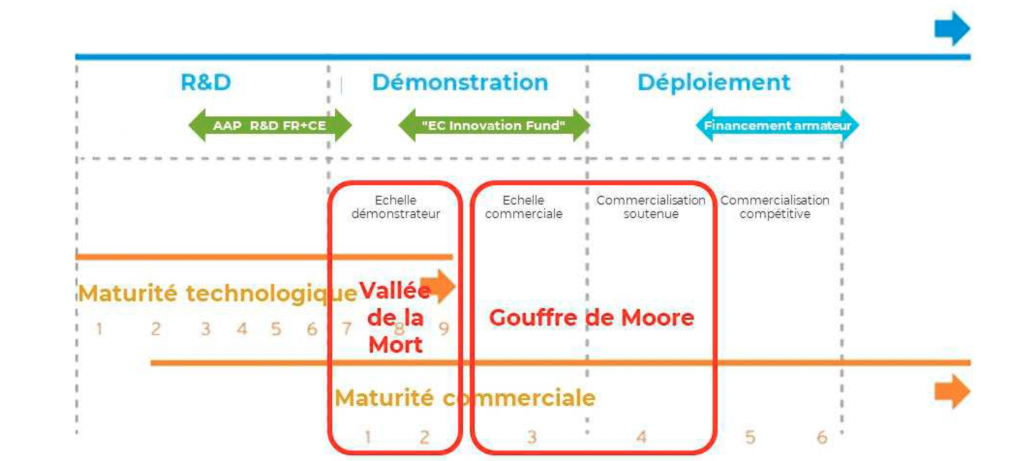

Current innovation aid mechanisms cover the upstream phases of new technological solution development (Technology Readiness Level / TRL < 7) well. However, these mechanisms are insufficient to cover the downstream phases:

7 https://www.oecd.org/finland/peer-review-finland-shipbuilding-industry.pdf

8 https://www.oecd.org/sti/ind/peer-review-netherlands-shipbuilding-industry.pdf

9 https://www.bmvi.de/SharedDocs/EN/Documents/MKS/mfs-strategy-final-en.pdf?__blob=publicationFile

10 https://www.bav.bund.de/DE/4_Foerderprogramme/7_Foerderung_LNG/Foerderung_LNG_node.html

11 https://www.bav.bund.de/SharedDocs/Downloads/DE/Bordstrom/Foerderrichtlinie.pdf?__blob=publicationFile&v=4

1. Full-scale demonstration of new technological solutions ( 7 ≤ TRL ≤ 9) :

Crossing the ‘Valley of Death’13, a term for the lack of ressources in the phase between desmonstrating a new technology and its first commercial success or market validation.

2. Achieving full industrial and commercial maturity for new green technological solutions:

Crossing the ‘Market Chasm’ (or ‘Moore’s Chasm’14), the transition between adoption by a first client (strategic buyer) in a pilot project and adoption by conservative mainstream customers who only buy fully mature products with solid references.

Crossing this market chasm is particularly critical for shipbuilding due to the sector’s specificities, especially in the current context of greening vessels.

12. The ratio of R&D costs to unit production costs is typically 1/10 for shipbuilding, whereas it ranges between 1/10,000 and 1/100,000 for other transport industries, particularly the automotive sector.

13. Yoshitaka Osawa & Kumiko Miyazaki (2006) An empirical analysis of the valley of death: Large‐scale R&D project performance in a Japanese diversified company, Asian Journal of Technology Innovation, 14:2, 93-116.

14. Moore, G. A. (1991) Crossing the chasm: Marketing and selling technology products to mainstream customers. / Rogers, E. M. (1962). Diffusion of innovations.

See the chart below illustrating these two critical downstream phases.

toward new financing mechanisms for large ‘green’ commercial vessels

The European maritime sector has set two major priorities to meet IMO and EGD objectives: (1) develop and validate by 2030 the solutions necessary for all types of vessels and maritime services to enable zero-emission shipping by 2050, and (2) strengthen the competitiveness of European maritime industries in the emerging green technology market.

The ‘Zero-Emission Waterborne Transport’ strategic partnership signed in June 2021 is a key instrument. However, the additional R&D funding it offers only covers the upstream portion (TRL ≤ 7).

The French sector has significant assets, including world-class players and pioneering R&D programs (notably CdA’s Ecorizon®). The French industry, and CdA in particular, has set an even more ambitious goal: to offer zero-emission vessels across the entire domestic production range by 2030, with deployment on smaller vessels as early as 2025.

The ongoing improvements to French innovation support (i_Demo) and European programs (ZEWT cPP, Innovation Fund) are a step in the right direction; however, they remain insufficient to enable the effective deployment of green equipment on board ships and to reach this objective. The required R&D effort, coupled with the unique characteristics of the naval sector highlighted above, calls for the implementation of new, more incentive-based financing mechanisms. These could be integrated into the France Relance plan and/or leverage private players in the energy sector subject to the CEE (Energy Savings Certificates) scheme.

15. Depending on the actual availability (in terms of volume, geographical distribution, and cost) of green maritime fuels (carbon-neutral or carbon-free) provided by energy suppliers.

>> creation of a Support fund for the installation of green equipment on large commercial vessels

This mechanism would benefit French construction, conversion, and repair yards for the development, design, supply, and integration of green technologies on new series and existing commercial vessels.

The intensity of the aid, its nature, and its terms of application are yet to be defined in detail, but they could be modeled after the European Innovation Fund (under DG CLIMA) or the tax tonnage/accelerated depreciation rules (suramortissement fiscal) currently benefiting French shipowners. Grant applications would be approved based on mature projects demonstrating high potential for GHG reduction.

Only additional costs related to green equipment would be eligible, covered at 40% before contract signature. The remainder would be disbursed as equipment is installed and based on GHG measurements during the first year of operation.

Funding for this instrument could be provided by the France Relance and France 2030 investment plans, which currently offer very little support to the shipbuilding sector compared to other industrial sectors. This funding would cover a period of at least five years starting from 2021, with a possible five-year extension depending on the green technologies available at that time. The inclusion of maritime transport in the Carbon Emissions Trading System (ETS) could also serve as a future funding source for this scheme, provided that a portion of the revenues is allocated to Member States.

The processing of applications could be entrusted to ADEME (the French Agency for Ecological Transition) on behalf of the State.

operating principle of the mecanism, see attached file

Overall budget required for this new mechanism: Projections of the Industry’s turnover for the next five years allow for an estimated total budget for this mechanism in the order of €1 billion over 5 years.

By way of comparison, the €8 billion Automotive Plan includes €150 million for R&D, but more importantly, €3 billion for aid toward the development and acquisition of new green technologies. This includes:

- €535 million in bonuses for electric vehicle purchases;

- €800 million in conversion premiums;

- €600 million for a support fund for automotive subcontractors;

- €200 million in investment for the modernization of the industry;

And nearly €850 million for the battery Gigafactory project by Saft, Stellantis, and Renault, united within the ACC (Automotive Cells Company) joint venture.

>> Extension of the energy savings certificate (cee) scheme to maritime sector

As the primary financing mechanism for the energy transition, the Energy Savings Certificates (CEE) scheme could be a compelling option to support investment in greening large vessels, by shifting part of the cost onto greenhouse gas-emitting energy suppliers. However, it is currently difficult to apply to the shipbuilding sector due to the scheme’s territoriality criteria. Indeed, only vessels operating direct routes between two French ports (Mainland France, Guadeloupe, French Guiana, Réunion, Martinique, Mayotte, and Saint-Pierre-et-Miquelon) are eligible for CEE-funded energy-saving operations.

The applicability of this scheme should be extended to all vessels manufactured in France, without navigation restrictions.

A dedicated calculation methodology for ‘Maritime CEEs’ could be developed based on global maritime CO2 emission reports (IMO’s ‘Data Collection System’) and/or European reports (EU Regulation 2015/757, known as the ‘Shipping MRV Regulation’).