PJL green industry

An industry mobilized to meet the Nation’s needs, with key points of attention to avoid discrepancies.

Proposal from french shipbuilding industry for the draft law on ‘green industry’

FEb. 2023

download the position paper

Backgroud information

The French shipbuilding industry is present throughout the country, with more than 750 companies and more than 830 establishments/sites, generating a turnover of £13.2 billion in 2021.

It is a very dynamic sector, with turnover growing by an average of 4% per year since 2014.

The industry employs more than 51,000 people, and it is estimated that there will be a net creation of 13,000 jobs across all regions by 2030.

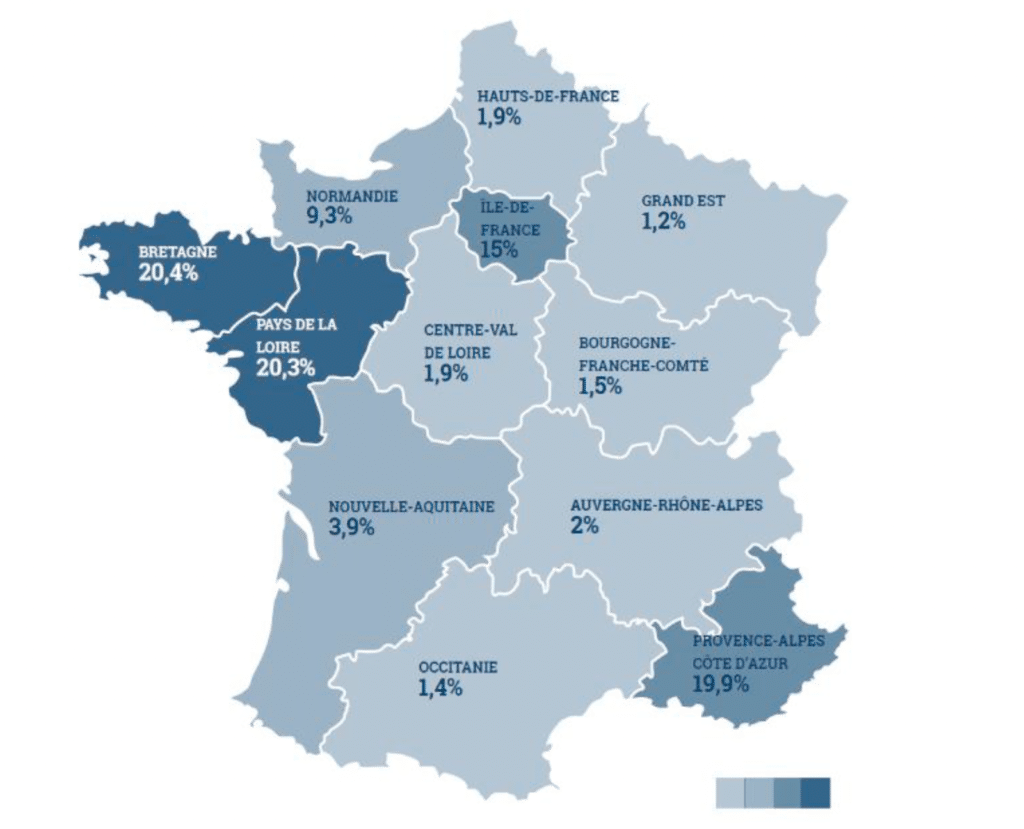

The sector has a strong presence in three coastal regions. 60% of its activity is carried out in Pays de la Loire, Brittany and Provence-Alpes-Côte d’Azur.

Investment in the construction of new industrial sites, the modernization of industrial facilities and the manufacture of equipment for ‘green’ ships are crucial challenges for the French shipbuilding industry. The shipbuilding industry is investing as much in its products as in its processes to significantly reduce its environmental impact and that of its products, in particular the carbon footprint over the entire life cycle of ships. To structure the work of manufacturers and guide public policy, the sector’s GreenShip technology roadmap sets the course for the necessary R&D efforts and serves as a reference document for the actions of the Maritime Industry Research and Innovation Steering Committee (CORIMER).

Beyond these R&D activities, the challenge lies in deploying and accelerating the industrial and economic maturation of these solutions. A joint State-industry consultation is underway to best support the construction and acquisition of decarbonized vessels (which entail a 10% to 20% cost premium compared to traditional ships), in compliance with new European and global regulatory requirements. Within the framework of the Climate and Resilience Act, efforts by the entire maritime sector and government bodies have developed and supported an action plan through a decarbonization roadmap, which complements the CORIMER technological roadmap.

While activity remains sustained and the sector continues to be highly dynamic, committed to the energy transition across all regions, the situation is complex. As a long-cycle industry, the shipbuilding sector is currently delivering vessels ordered several years ago. It must be noted, that in the order books of French and European shipyards are in decline both in absolute and relative terms, compared to those of Asian countries.

The shipbuilding industry welcomes the inclusion of the ‘Green Industry’ bill in the legislative agenda. Championed by the Minister for Economy, Finance, and Industrial and Digital Sovereignty, this bill dedicated to industrial issues and the reindustrialization of the national territory, the sector remains eager to see its own proposals integrated into these proceedings.

Gican proposals for the ‘Green industry’ bill

5 key Proposals:

- Transforming taxation to grow the green industry

- Simplification: Opening factories, rehabilitating brownfield sites, and making land available.

- Producing, commissioning, and purchasing in France.

- Financing the French green industry

- Training for green industry professions

transforming taxation to grow green industry

1.1 Implement Free Zones in overseas territories, similar to the Canary Islands Special Zone (ZEC), which has benefited from reduced taxation since 2000. This approach has developed the local naval industry, now representing 450 jobs and 100 million of euros in turnover, notably through the exemption of VAT and “dock dues” for industrial sites developed according to green criteria.

1.2 Align the Innovation Tax Credit (C2I) rate of 20% with the Research Tax Credit rate (CIR) of 30% to bolster industrial innovation.

1.3 Channel a larger proportion of French household savings (from Livret A) towards innovation and industry (via PER, life insurance, and increasing investment caps for FCPI funds beyond 15 million euros per company).

1.4 Integrate incentives to use French industry within investment support schemes for green vessel purchases (accelerated depreciation, leasing, and guarantees.)

Simplification / opening factories and land availability

2.1 Finance the construction of port, naval, and river infrastructure to develop French green shipbuilding and Marine Renewable Energies (MRE), specifically the AGORA project in Saint-Nazaire. France lacks infrastructure for medium-sizes hulls. The closure of the Ateliers et Chantiers du Havre in 1999 deprived the country of the most relevant facilities for this scale. This deficit leads to ‘green’ project leaking to foreign competitors, such as the NEOLINE project, which will be largely built in Turkey.

2.2 Support the innovation and industrialization of industrial start-ups.

- Multiply industrial ‘third places’ by mapping and capitalizing on existing sites where entrepreneurs can find workshops, consultancy, and access to machine tools.

- Deploy insurance protecting against abusive legal appeals against start-up construction projects, with premiums co-financed by BPI France.

- Establish free zone systems and tax holidays for the factory launch period, including guarantee and counter-guarantee systems.

2.3 Establish a ‘green industrialization’ support scheme to help define the environmental strategy for upcoming projects, such as a first factory or operational launch.

2.4 Consolidate the shipbreaking and recycling sector to guarantee its scale-up in increase recycling rates, fostering a circular economy within the naval industry. Identify specific territories for these yards to expand.

Producing, commissionning, and purchasing in France

3.1 Ensure that public funds (PIA, ERDF) and public bodies (AFD) exclusively finance project led by French industrial players with a mandatory high percentage of national content, preventing French funding from benefiting foreign competitors.

3.2 Centralize the oversight of public vessel procurement for French administrations under the General Secretariat for the Sea (SGMer).

3.3 Guarantee that all sectors covered by bids respect the criteria of Articles L.2153-1 to L.2153-5 of the Public Procurement Code.

3.4 Use public procurement to support innovation and first orders of decarbonization solution by :

- Systematically including eco-design approaches based on the highest standards for State or local authority vessels.

- Requiring a minimum of 20% of the vessel’s value to be dedicated to decarbonation equipment in public tenders.

3.5 Allocate France 2030 credits for the direct procurement of innovative energy transition solutions from emerging players.

3.6 Integrate carbon footprint criteria for the construction of vessels used in offshore wind farms within the MRE deployment policy.

Financing the french green industry

4.1 Create a support fund for financing line for the installation of green equipment. This would benefit French shipyards (construction, conversion and repair) for the design and integration of green technologies on new and existing commercial series. 40% of the green ‘extra cost’ would be covered before contract signing, with the remainder disbursed based on verified Geenhouse Gas (GHG) Savings after the first year of operation.

4.2 Simplify access to France 2030 founds for R&D, innovation, and industrialization via state operators (ADEME, Bpi France).

4.3 Provide CORIMMER with its own budget and dedicated human resources.

4.4 Establish structural projects to develop industrial sectors focused on decarbonization levers (wind propulsion, electric hybridization, hydrogen storage, etc).

4.5 Balance revenues generated by new maritime regulations (EU ETS, Fuel EU Maritime) with support for stakeholders to invest in decarbonization.

4.6 Encourage integrated offshore wind farms that include hydrogen bunkering facilities for vessels at the base of the wind farm.

training for green industry professions

5.1 Implement the FORTEIM Project to evolve specific industry training towards the energy transition and offshore wind development.

5.2 Mandate training on the eco-energy transition and industrial environment knowledge starting from secondary education.

5.3 Increase awareness of the industry among private investment funds by communicating its specificities and financial needs (matching TRL/MRL) levels with funding).

5.4 Launch awareness actions for private and public decision-makers (CEOs, board members, clusters) regarding the energy transition across the maritime sector.